BVARs vs. TSFMs: Priors, Shocks, and the New Forecasting Stack

Bayesian VARs and time series foundation models solve different forecasting problems: BVARs encode structural priors and scenarios; TSFMs scale zero-shot forecasts across heterogeneous series.

Bayesian vector autoregressions and time series foundation models are easy to frame as old versus new. BVARs come from macroeconometrics: equations, lags, priors, posterior draws, impulse responses. TSFMs come from the foundation-model era: transformers, pretraining corpora, zero-shot inference, model routing. The surface comparison makes TSFMs look like the natural replacement.

That is the wrong framing.

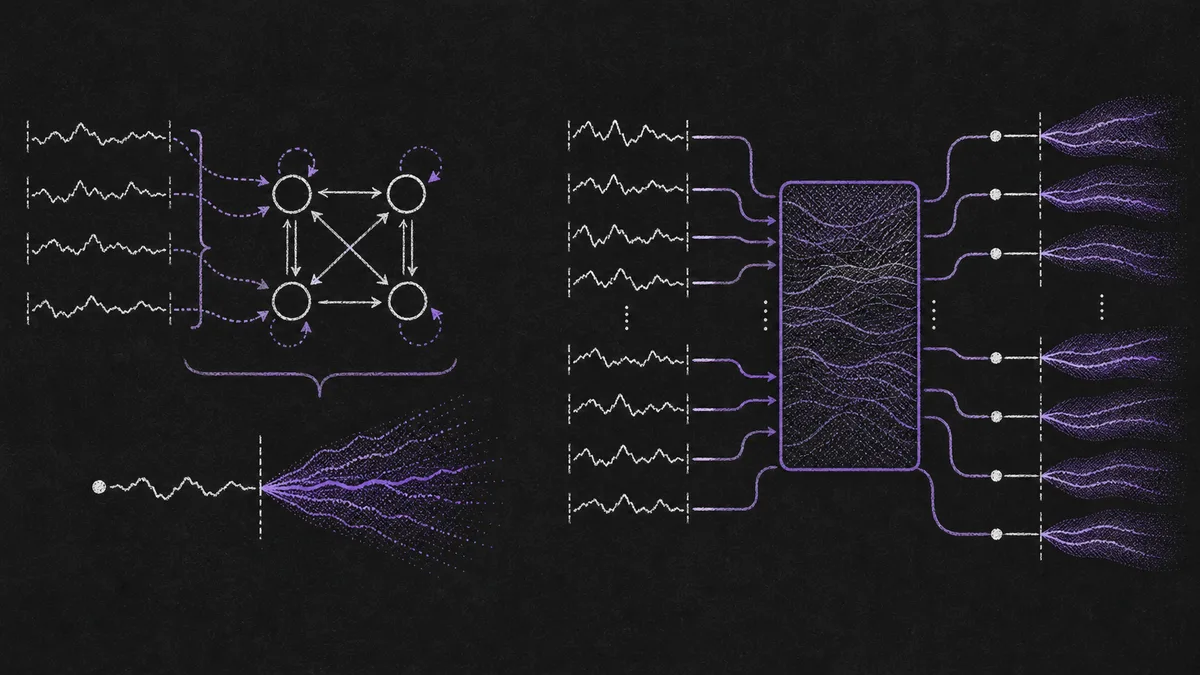

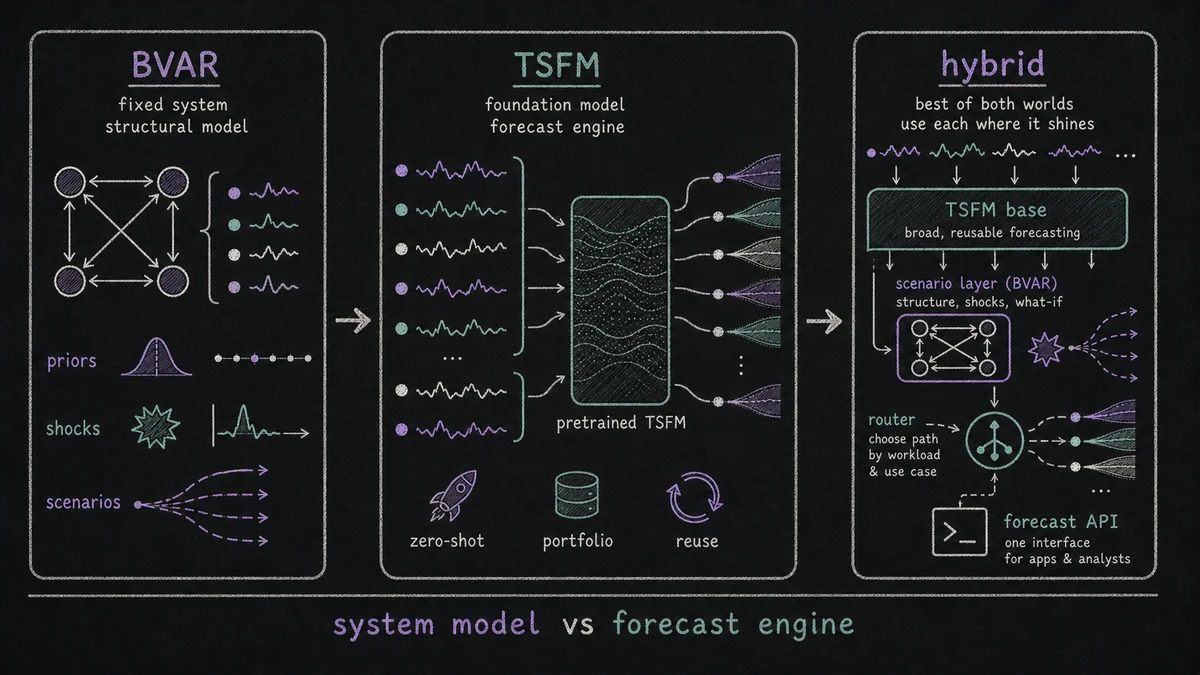

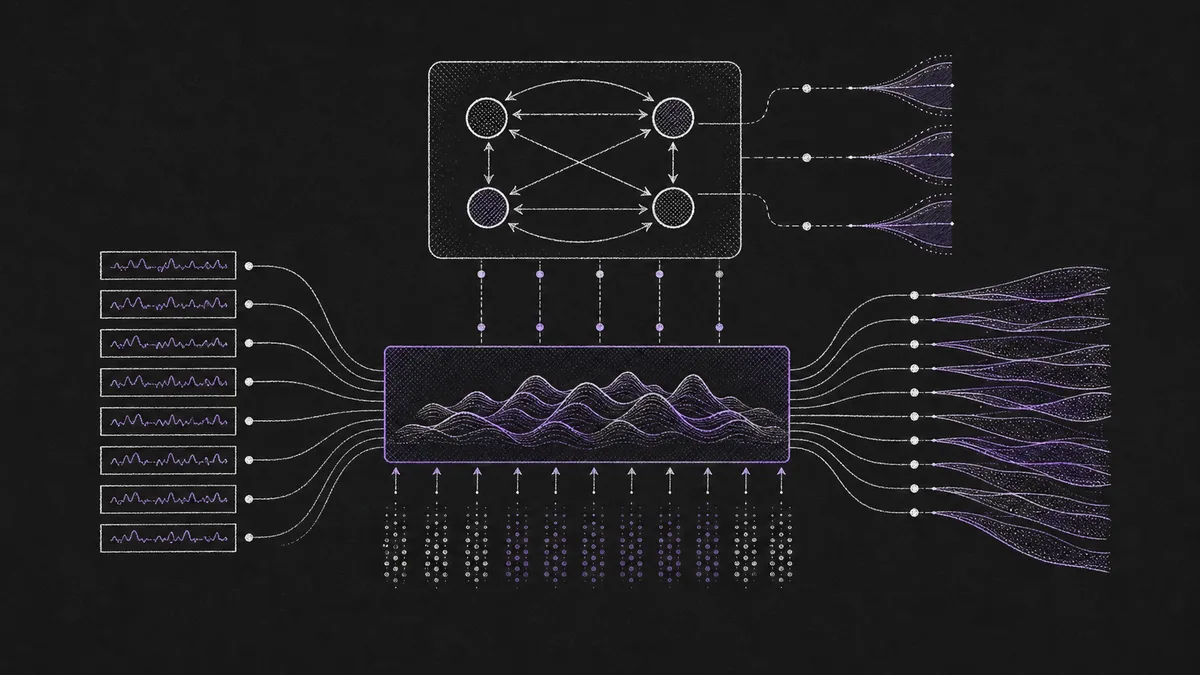

BVARs and TSFMs solve different problems. A BVAR is a disciplined way to forecast and reason about a fixed system of related variables when the variable set is known and the analyst cares about shocks, uncertainty, priors, and scenarios. A TSFM is a pretrained forecasting engine that can be applied across many heterogeneous time series without fitting a model for each one. BVARs are strongest when the system is small enough to think about. TSFMs are strongest when the forecasting portfolio is too large, messy, or fast-moving for bespoke modeling.

The useful question is not "which model wins?" It is: where should each sit in the forecasting stack?

#What a BVAR Actually Buys You

A vector autoregression models a vector of variables as a function of its own lagged history:

y_t = c + A_1 y_{t-1} + ... + A_p y_{t-p} + epsilon_t

If the vector is [inflation, unemployment, interest_rate, output_gap], every variable is allowed to depend on lagged values of every other variable. That makes VARs flexible, but it also creates a parameter problem. With k variables and p lags, the coefficient count grows quickly. A modest 20-variable, 4-lag VAR already has thousands of coefficients before adding covariance parameters.

BVARs solve this by putting priors on the coefficients. The classic Litterman / Minnesota prior shrinks the model toward a simple benchmark: each variable is mostly explained by its own recent past, cross-variable effects exist but are smaller, and longer lags matter less. Later work such as Large Bayesian VARs showed that shrinkage lets VARs absorb much larger macro panels without collapsing under estimation noise. Giannone, Lenza, and Primiceri pushed this further by treating prior tightness as something to estimate rather than a purely subjective knob.

That gives BVARs three durable advantages:

| BVAR strength | Why it matters |

|---|---|

| Explicit priors | Domain knowledge can be encoded directly rather than learned implicitly |

| Joint dynamics | The model forecasts variables together, not as isolated series |

| Posterior simulation | Forecast uncertainty, scenarios, and impulse responses come from the same object |

This is why BVARs remain workhorses in central banking and macro forecasting. A policy team does not only ask "what is inflation next quarter?" It asks what happens if rates rise, which variables move first, how uncertainty fans out, and whether the forecast is consistent with a coherent macro story. A BVAR is built for that conversation.

#What a TSFM Buys You Instead

TSFMs make a different trade.

Models such as TimesFM, Chronos, and Moirai are pretrained on large collections of time series. At inference time, they can forecast a new series without fitting a new model. GIFT-Eval formalized this evaluation setting across domains, frequencies, horizons, and multivariate inputs.

The operative word is not "Bayesian" or "structural." It is reuse. The pretraining cost has already been paid. The model has learned broad temporal patterns: trend, seasonality, intermittency, volatility, changepoints, multi-scale recurrence. A practitioner can send a history window and receive a probabilistic forecast immediately.

That gives TSFMs a different set of advantages:

| TSFM strength | Why it matters |

|---|---|

| Zero-shot inference | No per-series fitting loop for every target |

| Cross-domain reuse | One model can cover retail, energy, finance, sensors, traffic, and more |

| Cold-start behavior | Useful forecasts can begin with little target-specific history |

| Operational simplicity | Serving can be centralized behind a forecast API or model router |

This is the terrain covered in our traditional forecasting vs. TSFM lifecycle post. TSFMs compress the build-maintain-retrain cycle. When you have 50,000 SKUs, 20,000 infrastructure metrics, or thousands of regional demand series, the cost of fitting and governing a bespoke model for each target becomes the problem. TSFMs attack that operational burden directly.

#The Core Difference: System Model vs. Forecast Engine

The cleanest distinction is this:

| Question | BVAR answer | TSFM answer |

|---|---|---|

| What is being modeled? | A fixed vector system | A reusable temporal pattern distribution |

| How is knowledge injected? | Priors and variable choice | Pretraining data and architecture |

| What changes per deployment? | The fitted posterior | Mostly the input context |

| Best unit of work | One coherent system | A large portfolio of series |

| Best explanation object | Coefficients, shocks, impulse responses | Forecast distributions, examples, routing diagnostics |

BVARs are system models. You decide which variables belong together, specify lag structure and priors, estimate the posterior, and use that posterior to forecast and analyze the system.

TSFMs are forecast engines. You do not usually specify the economic or physical system explicitly. You provide observations and ask the pretrained model to infer the local pattern from context, using priors learned from broad pretraining.

This is why a BVAR can be better for four macro variables and worse for 40,000 operational metrics. It is also why a TSFM can be excellent for an API-driven forecast portfolio and still be the wrong tool for a monetary policy shock decomposition.

#Where BVARs Still Beat TSFMs

Scenario analysis with known variables. If the user asks, "what happens to unemployment and inflation if policy rates rise by 100 basis points?" a BVAR has a natural answer. Conditional forecasts and structural VAR extensions were designed for exactly this kind of exercise. A TSFM can forecast under a modified input path if covariates are supported, but that is not the same as identifying a structural shock.

Small systems with high stakes. A five-variable macro model may be more useful than a large black-box forecast if the cost of a wrong explanation is high. Finance, central banking, insurance, and regulated planning often need a forecast that can be defended in terms of assumptions, priors, and sensitivity.

Data-poor but theory-rich domains. If you have limited observations but strong beliefs about persistence, long-run means, or cross-variable signs, a BVAR lets you encode those beliefs. TSFMs rely on pretraining priors, which may or may not match the domain.

Coherent joint uncertainty. BVAR posterior draws produce joint paths across variables. This matters when downstream decisions depend on combinations of variables: inflation and rates, demand and price, unemployment and output. Some TSFMs produce excellent marginal forecast distributions, but coherent joint scenario distributions are still uneven across model families. Our multivariate forecasting overview walks through why cross-variable modeling remains hard.

#Where TSFMs Beat BVARs

Large heterogeneous portfolios. BVARs need a defined variable system. Forecasting thousands of unrelated or weakly related series with BVARs usually means either many small models or a very large sparse model. TSFMs handle this pattern naturally: each series or series group can be sent through a shared forecasting service.

Cold starts and new targets. A BVAR cannot estimate cross-variable dynamics for a new series with almost no history unless the analyst supplies strong structure. A TSFM can often produce useful zero-shot forecasts from short context because its prior comes from pretraining, not only from the target series.

Messy operational data. Retail, infrastructure, web traffic, sensor, and logistics series frequently violate the clean assumptions macro models prefer. Missing values, irregular behavior, mixed frequencies, promotions, outages, and catalog churn are normal. TSFMs are not magic, but their learned pattern library is often more forgiving than a hand-specified VAR.

Speed of deployment. BVARs require model design: variable selection, transformations, lag length, prior calibration, posterior computation, backtesting. TSFMs shift much of that effort into a single inference call. This is why a model routing layer becomes valuable: the system can try multiple foundation models and choose the best performer for each series family.

#The Trap: Treating TSFMs as Structural Models

TSFMs learn statistical regularities. That does not make them causal models.

This distinction matters because the output often looks authoritative. A TSFM can produce a forecast interval for inflation, energy load, or sales. It may even respond sensibly when you include covariates, as discussed in our covariates guide. But unless the model and inference procedure are explicitly designed for intervention, it is still estimating a conditional predictive distribution, not a policy counterfactual.

That is exactly where BVARs retain value. Structural assumptions may be imperfect, but they are visible. A BVAR forces the analyst to say what variables are in the system, what lagged relationships are allowed, what is being shrunk, and how shocks are identified. TSFMs often hide their priors in pretraining data and weights.

The right mental model is:

| Use case | Default choice |

|---|---|

| Forecast 10,000 product or metric series next week | TSFM |

| Explain a policy shock across macro variables | BVAR / SVAR |

| Fast baseline for a new time series product | TSFM |

| Regulated scenario forecast with a fixed variable set | BVAR |

| Domain with many weakly related targets | TSFM |

| Domain with few strongly theorized variables | BVAR |

#The Hybrid Stack

The strongest production architecture will often use both.

A practical hybrid stack looks like this:

- Use TSFMs as the default forecast layer. Every series gets a strong zero-shot or routed foundation-model forecast. This covers the long tail and eliminates the per-series modeling burden.

- Use BVARs for structured systems. Macro panels, financial factor systems, energy market variables, and other coherent variable groups get BVAR or structural VAR treatment.

- Compare forecasts where they overlap. If both a TSFM and BVAR forecast the same macro variable, disagreements are useful. A TSFM may catch nonlinear pattern similarity; a BVAR may preserve economically coherent relationships.

- Feed scenarios downstream. BVAR scenario paths can become inputs, benchmarks, or stress cases for the operational forecast layer.

- Keep governance separate. Do not pretend the TSFM explains shocks, and do not pretend the BVAR can handle every noisy operational series.

This is the same convergence pattern we see in broader forecasting stacks: foundation models become the baseline, while traditional methods survive where their assumptions are assets rather than liabilities.

#A Concrete Example

Imagine an energy retailer forecasting demand, prices, weather-sensitive load, and financial exposure.

The TSFM layer forecasts thousands of customer load series, feeder-level demand traces, meter clusters, and regional operational metrics. It handles cold starts for new customers and provides quick forecasts for long-tail segments. The model router chooses among Chronos, TimesFM, Moirai, or specialized energy models depending on series shape.

The BVAR layer models a smaller system: wholesale price, load, gas price, renewable generation, temperature, interest rates, and maybe a few macro indicators. It is used for stress tests and scenario planning: what if gas prices spike, temperature deviates from seasonal norms, or rates move faster than expected?

The two layers answer different business questions. The TSFM says what the portfolio is likely to do. The BVAR says how a coherent set of drivers might move together under a scenario. One is breadth; the other is structure.

#Bottom Line

BVARs are not obsolete because TSFMs exist. They are narrower, more explicit, and more useful for structured systems than broad portfolio forecasting. TSFMs are not automatically better because they are newer. They are broader, faster to deploy, and better suited to heterogeneous forecast portfolios, but they do not replace structural thinking.

The practical rule is simple:

| If the work is mostly... | Start with... |

|---|---|

| Forecasting many series | TSFM |

| Explaining a fixed system | BVAR |

| Cold-start operational forecasting | TSFM |

| Scenario analysis and shocks | BVAR |

| Model governance and assumptions | BVAR |

| Fast deployment and scale | TSFM |

The new forecasting stack should not choose one tradition and discard the other. It should let BVARs do what they are good at: encode priors, model joint systems, and support scenario reasoning. It should let TSFMs do what they are good at: make strong forecasts across diverse time series without bespoke fitting. The teams that get this right will not argue about BVAR versus TSFM. They will route each forecasting question to the model class that was built for it.

Primary sources: Litterman, "Forecasting with Bayesian Vector Autoregressions" · Bańbura, Giannone, and Reichlin, "Large Bayesian VARs" · Giannone, Lenza, and Primiceri, "Prior Selection for Vector Autoregressions" · TimesFM · Chronos · Moirai · GIFT-Eval